Q2 State of the Venture Capital Market

Venture capital is constantly evolving with a new variation emerging every few years. We recently emerged from an era of hyper-activity – marked by an extraordinary surge in deals, valuations, and capital inflows – that the entire ecosystem is still recalibrating from. As a result, in Q2 we continued to see a contraction in funding rounds, lower valuations, and a more cautious approach from investors.

This year we’ve observed a more measured and sustainable pace to VC investments. As we step out of Q2 2024, there are promising signs that stability and growth have returned to the venture capital market.

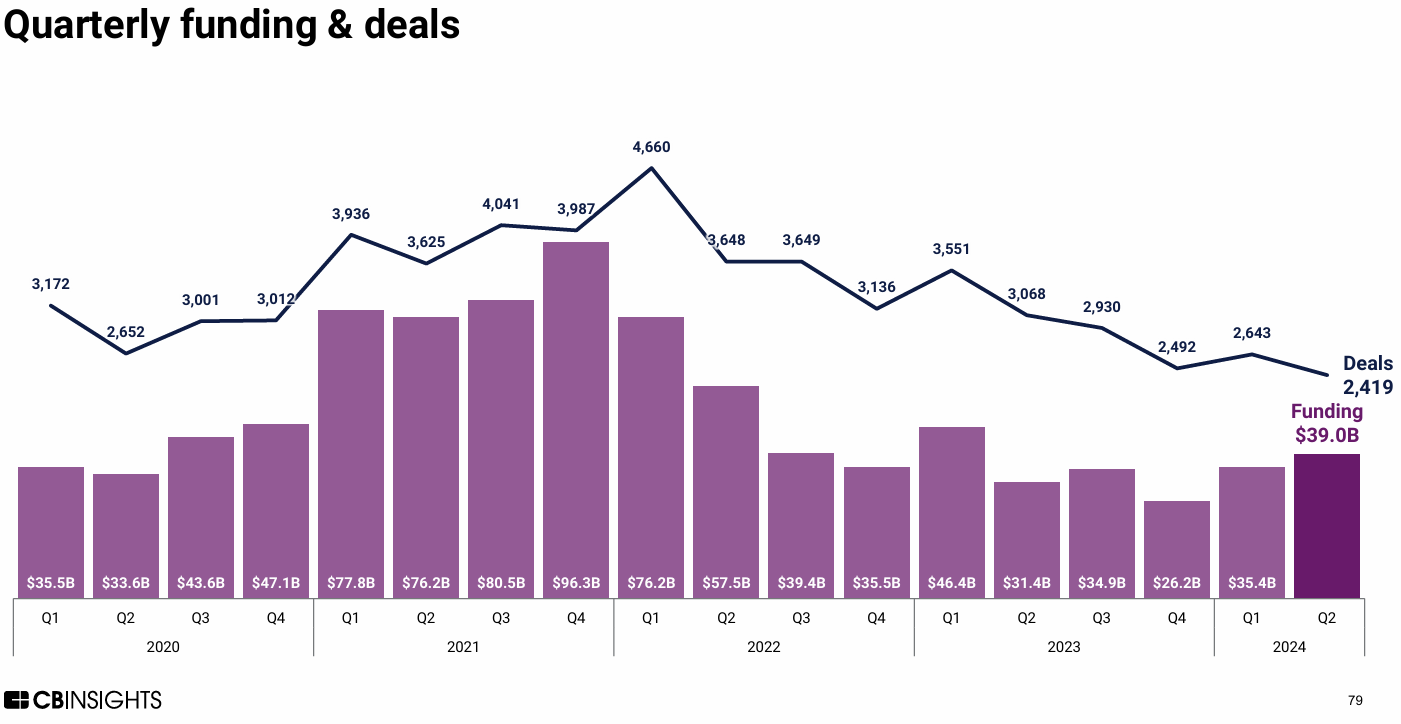

Q2 was a healthy quarter for venture capital. Global venture capital activity was $65.7B in Q2, with the US accounting for $39.0B – the second consecutive quarter for growth. We have entered a stable phase which we at Cervin Ventures think is healthy for the industry. Public market multiples have normalized at levels lower than the 2019-20 period. M&A deal count has increased from the last quarter, with fluctuations remaining within 5% since early 2023.

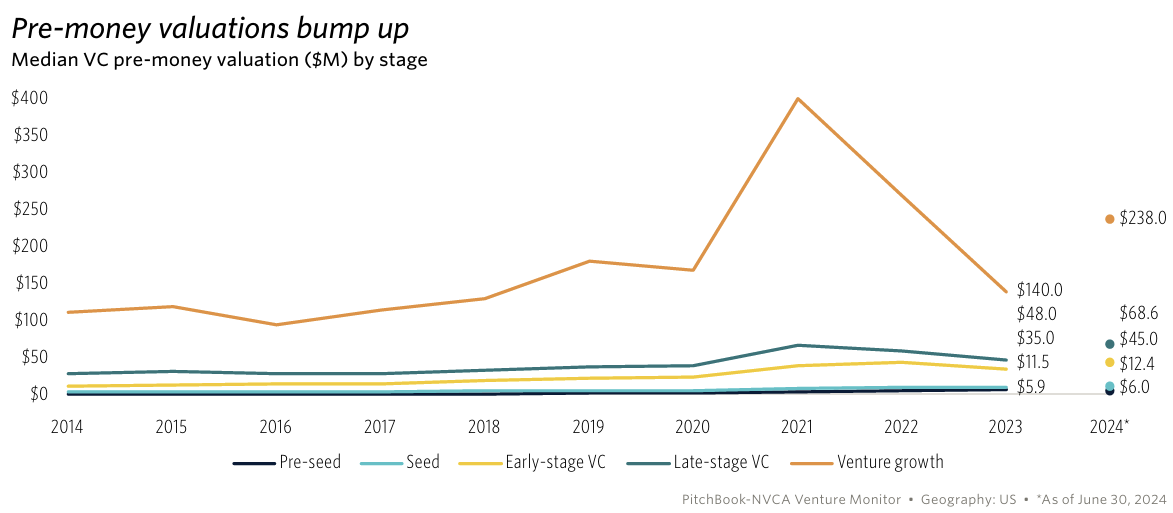

Early-stage deal counts in the US have reached the highest since Q1 2022. While Pre-Seed and Seed deal sizes have remained consistent over the past 2 years, there is a significant increase in deal size across early, late and growth stages. Pre-money valuations have seen some significant step ups from 2023 to 2024.

Artificial Intelligence and Machine Learning

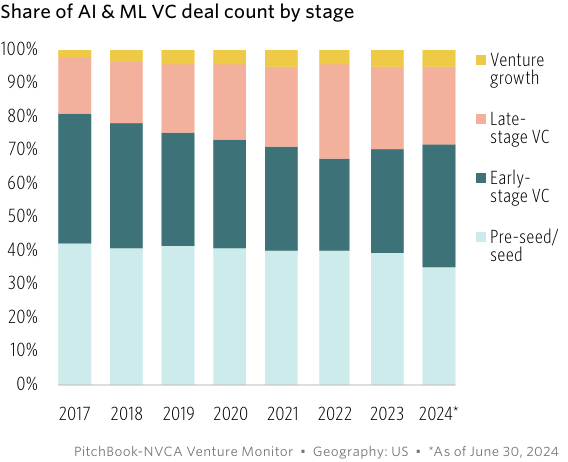

Early-stage startups continue to dominate the AI & ML deal count.

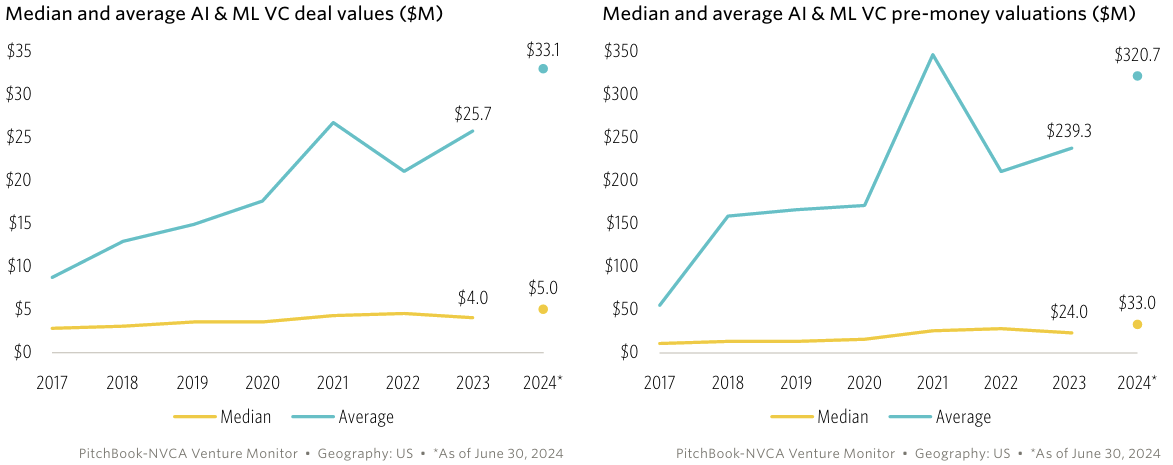

The steep price tag of the AI Infrastructure buildout has increased the demand for capital. As a result, average deal sizes and valuations of AI leaders are rising too. In recent quarters, AI-enabled vertical applications have seen the highest deal volume and overall funding within the AI/ML segment. Foundational or horizontal applications on the other hand have seen fewer deals but larger deal sizes and valuations. We continue to believe that vertical applications will be the area where smaller funds like Cervin will be able to add value.

Average AI deal values have jumped from $25.7M to $33.1M from 2023 to 2024. This is roughly a 29% increase YoY. In comparison, average pre-money valuation has risen from $239.3M to $320.7M (34% YoY). The median deal value and pre-money valuations rose at 25% and 37.5% YoY respectively.

Q1-Q2 2024 saw 8 VC deals in AI/ML larger than $1B; whereas Q3-Q4 2023 had just 4 such deals. Larger deals, like CoreWeave, xAI, and Anthropic, are inflating the valuation and deal value numbers for the entire AI segment.

The industry continues to offer higher valuations and revenue multiples to AI/ML companies-which is ultimately resulting in higher increase in the pre-money valuations. There are fewer, but larger deals happening, with a premium being offered to AI researchers.

Portfolio News

We welcomed the following new companies to our portfolio in Q3.

Airgap Networks, an innovator in agentless segmentation for enterprise IT and OT environments, has been acquired by Zscaler (NASDAQ: ZS). With this acquisition, Zscaler will combine its Zero Trust SD-WAN with Airgap to extend the Zero Trust Exchange to protect east-west traffic in branch offices, campuses, factories, and plants with critical OT infrastructure.

Anvilogic raised a $45M Series C funding round. Anvilogic's AI-based Multi-Data Platform SIEM is breaking the vendor lock-in that drives detection gaps and high costs for enterprise security operations, enabling teams to detect, hunt, and investigate threats across the data platforms they choose. Our additional investment reflects our confidence in Anvilogic's vision and their ability to drive innovation in the cybersecurity space, particularly with their generative AI features in the SOC.

![]()

Bolster raised a Series B round of funding, with M12, Microsoft’s venture fund, leading the round. With over $40M raised in total, they’re charging ahead to deliver multi-channel threat protection to defend against phishing and impersonation attacks.